Part 6

The quest for alpha at Evovest

At Evovest, our main goal is to predict alpha, or relative returns, by combining our knowledge of the behavior of the stock markets with artificial intelligence. We aim to be accurate, and our measure of accuracy is defined as being better than randomness with consistency over a long period of time.

One of our greatest strengths is our awareness of the ignorance factor in our investment process. We explain our view about this in Part 4. As we evolve, we strive to increase the available information constantly by our continuous research and development efforts. Let us tell you how we address this R&D issue.

Forecasting alpha comes with a level of uncertainty. We know that some of it exists by the random characteristic of the stock markets and some of it exists because we just don’t have the full picture at any given time.

Recognizing that our prediction is imperfect, decomposing it into a function of external unknown informative elements and a random error gives us a framework to work with.

Recognizing that our prediction is imperfect, decomposing it into a function of external unknown informative elements and a random error gives us a framework to work with.

Looking at our investment process, we can share that among other things, our known informative elements include the following:

· Historical financial ratios · Firm characteristics · Macroeconomic data

· Analysts’ expectations · Technical indicators · CorrelationsSimply stated, our main goal is to model the alpha for stocks using those known informative elements combined with artificial intelligence.

We have developed strong scientific processes that mitigate biases in building a systematic investment strategy. The tools go from cross-validation to algorithm design while adopting a strong intellectual integrity. Going through a robust assessment of past observations, our investment process develops an experience and is retrained to reassess new information.

By focusing on predicting alpha and taking a holistic view, we have a process that can adapt to the ever-changing markets conditions, and we do not display a style bias over the medium/long term. As we introduced in Part 5, most of our alpha isn’t replicable by factor investing.

Some would use the term manager’s skills to define the capacity to produce non-replicable alpha. We believe this is a solid competitive advantage of ours and take pride in our stock picking capability. The investment process will forever continue to evolve, and this gives us strong confidence in our ability for the future.

Before showcasing some of our results in upcoming parts, note that hiring us doesn’t end with what we have accomplished, but includes what we will achieve. As we introduced the framework we work with, we highlighted that we’re aware of informative elements that we don’t consider. A few examples:

· Qualitative assessment · Management discussions · News sentiments

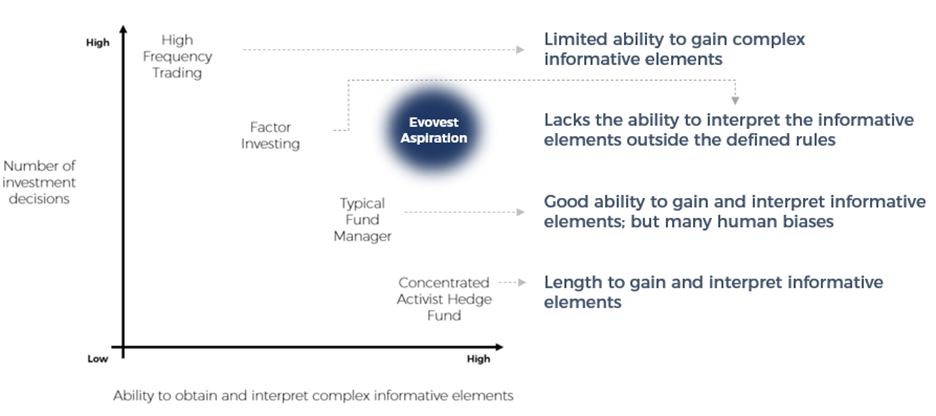

· Market research · Transcript data · Etc.We have a clear R&D path to ingest more unknown informative elements in our investment process. We consider this is the key for us to continue to stand out. As we add more and more informative elements in our investment process or by adding new machine learning algorithms, we believe our journey will enable us to make more informed decisions. Introduced in Part 2 of the discovery series, the next figure illustrates our aspirations.

Figure 1 – A framework for investment approaches and our destination

In the future, we will share with you how we use our predictions to make investment solutions as we segregate the alpha signal from the portfolio optimization process.

In the future, we will share with you how we use our predictions to make investment solutions as we segregate the alpha signal from the portfolio optimization process.

For more details about our investment process, we would be pleased to have a discussion with you. Our contact information is on our website evovest.com.