Part 4

Awareness in financial markets - Knowing we miss information

Awareness is an interesting concept in financial markets because most of the participants will say they know their investments inside out but, most of the time, they will fail to describe what they don’t know. This part is about shining light on this paradox while highlighting the limits of awareness by exposing the opposite of it: ignorance.

We believe being aware of what informative elements we are missing gives us insights into building a better investment process. While, it may seem very theoretical, this addition to our framework gives us the essential tool we need to keep our evolution the central piece of our future development and not forever operate under bounded rationality.

Referring to different investment styles, firms will be using different informative elements and having their own interpretation to maximize alpha prediction. The natural question that follows is: How do we take into consideration what is ignored into the decision? Let’s start by comparing two styles: concentrated and factor investing.

The concentrated portfolio manager will spend an enormous amount of resources to understand every aspect of the business model and evaluate the competition to find ways of unlocking long-term value. They will mostly ignore any signals the high-frequency trading firms will spend resources on.

On the other hand, factor investing firms will have a rule-based approach, using broadly available financial data to build financial ratios and rank securities. Thereafter, the decision will be based upon the rankings, while ignoring the business model, the competition, and the technical trading signals.

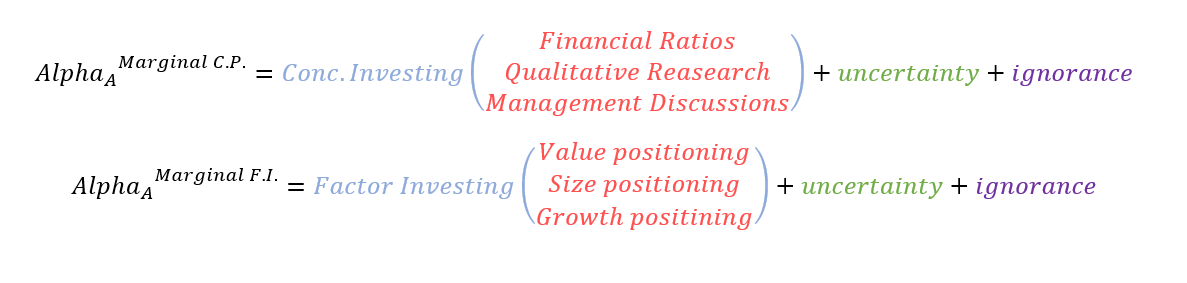

At this point, it should be clear that the ignorance of some informative elements is being showcased by many market participants. Continuing with the equation framework we had in the previous part, we can further break it down in 4 sections:

The part in red can be interpreted as the most important informative elements the investment style takes into consideration.

The part in blue is the style applied to the information, we can have two different styles applied to identical inputs.

The part in green is what we are unable to predict, a form of unknown unknown accompanied with a randomness effect.

The part in purple is the known unknown, key informative elements ignored.

To complete, we are giving an example of what two different investment styles looks like using our framework.

Let’s elaborate on the last part of the equation. As we recall, investment is all about making choices. Ignorance plays a central part whether it’s chosen on purpose or by laziness. The choice to ignore is a form of awareness. A natural question is: why does it matter?

Let’s elaborate on the last part of the equation. As we recall, investment is all about making choices. Ignorance plays a central part whether it’s chosen on purpose or by laziness. The choice to ignore is a form of awareness. A natural question is: why does it matter?

We think this gives a much-needed addition to our framework to understand investment biases in general. We would like to remind our readers how diversified the market participants are. For those having CNBC or Bloomberg TV open in the background while working, you can hear investment shows telling people:

“When fundamentals are murky, I like to fall back on technical analysis, markets are a buy right now.”

“The Dow Jones is struggling to support on here, around that 50-day moving average, we would not be buying here.”

“We are confident about a turnaround in inventory and consumer demand, a confirmation the economic data should give us this week, buy the dip.”

“We are not buying the dip here, because there is a recession risk.”

This should give our readers a sense of how this plays out daily. Those quotes were taken a few days apart. They should have presented the same information. We see how the investment style combined with the awareness of the different informative elements can give diverging perspectives.

At Evovest, our awareness of our ignorance is present in our continuous R&D efforts. This characteristic is central to the service we offer. By knowing we lack information, we can have a plan to diminish its possible negative effects and work towards an architecture that aims to include as much informative elements as possible.

To summarize our framework at this point:

We have a simple problem to solve, which is to accurately predict the alpha of stocks to build an investment portfolio.

This task is a function of how well we can obtain and interpret different informative elements and the amount of investment decisions we can make out it.

Obtaining and interpreting the same information can give different results based on the investment style the market participants apply.

Market participants often ignore important pieces of informative elements based on their preferences.

The next part of the discovery series will be a critic of factor investing, which we are too often compared to. We will highlight how we are able to extract more information than a simple rule-based investment strategy by using state-of-the-art machine learning methods.