Part 2

Driven by quantity and ability – A framework for investment approach

Part 1 introduced the quest for alpha by presenting the need to make choices in active management. We now continue by looking at its paradigm with two key elements: quantity and ability.

Investment decisions can be simplified by many forms, but we like to think of them in those two terms, which relate easily to the theory behind the law of active portfolio management¹.

We will base our framework on this theory since it gives us a simple but elegant way to illustrate our thoughts. We can decompose it using two axes.

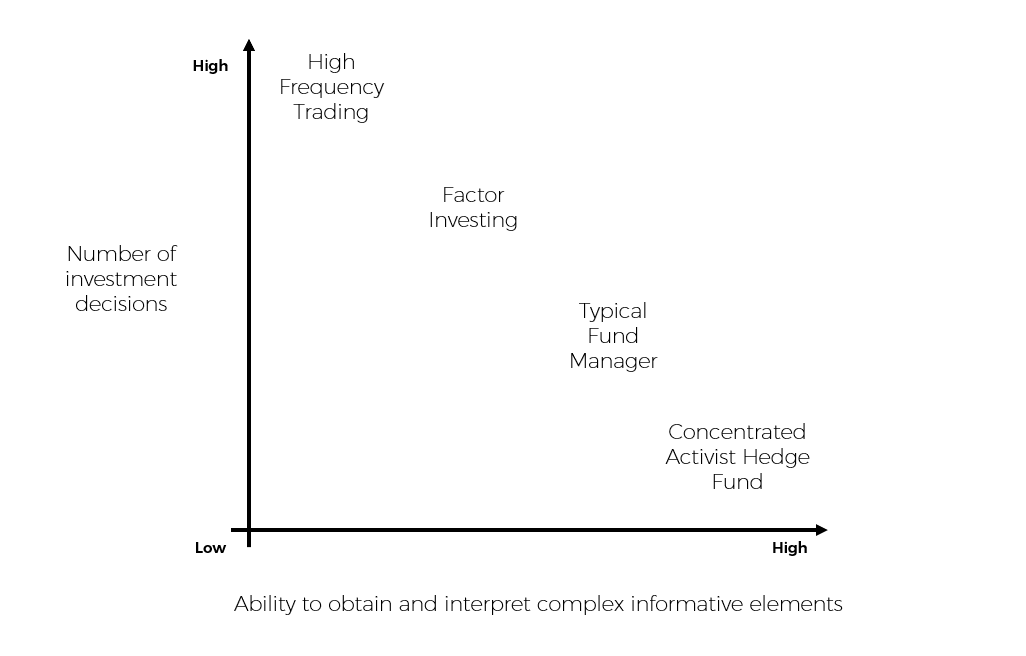

The first axis is the amount of investment decisions an advisor can make in a specific time horizon.

The second axis is the ability of the advisor to obtain and interpret complex informative elements. We see this as directly related to the potential success of an investment decision. The higher it is, the greater the expected alpha should be.

Using this, we can create a graphical representation of some market participants. As Figure 1 illustrate:

High frequency trading firm makes a massive amount of investment decisions while having a limited ability to gain complex informative elements.

Factor investing process is a rule-based method that can yield an important number of investment decisions, but the rules are often simple. This framework also lacks the ability to interpret the informative elements outside the defined rules.

The typical human advisor managing a mutual fund can make a less important amount of investment decisions but has a good ability to gain and interpret complex the informative elements.

The concentrated activist hedge fund will make few investment decisions but will go great length to gain and interpret the informative elements.

Figure 1 – A framework for investment approaches

In theory, we believe that an investment approach where you can make a lot of investment decisions combined with a high ability to obtain and interpret the informative elements should have a high degree of attractiveness for an investor. This comes down to the fact the combination should give a better probability to create alpha than the opposite.

In theory, we believe that an investment approach where you can make a lot of investment decisions combined with a high ability to obtain and interpret the informative elements should have a high degree of attractiveness for an investor. This comes down to the fact the combination should give a better probability to create alpha than the opposite.

Coming back to our quest for alpha in the previous part, we now have a way to assess divergent investment approaches from one another. However, this framework lacks depth since it does not give any insights into how two similar approaches can result in different investment views. We distinguish between the investment approach, just introduced, and the investment style, for which we will use the popular classification. The style can be seen as a subcategory of the approach. For example, the factor investing approach can by broken down for many styles that include value, growth, size, momentum, and quality to name a few.

In the next part, we will add to this framework with an additional perspective on the different type of abilities and biases creating the diversity of the market participants.

Law of active portfolio management can be referred as Information Ratio = Information Coefficient*√Breadth, where the information coefficient relates to the ability to obtain and interpret complex informative elements, the information ratio is the added value in every unit of risk added and breadth is the amount of investment decisions made.